Why SBF’s demise proves we need the blockchain

Plus, what the film "Quiz Show" can teach us about our faulty heuristics

You’re probably tired of hearing about Sam Bankman-Fried (SBF). I certainly am.

For many of my readers, FTX’s collapse officially marked crypto “deceased”. Based on how the FTX collapse has been portrayed in the media, declaring crypto “deceased” is understandable.

The problem with the majority of the media takeaways thus far is they ignore the obvious: blockchain could have prevented this disaster.

While nothing regarding crypto has anything to do with the failure of FTX, the dark paint splatters on the industry are as precise as Jackson Pollock.

In fact, FTX’s demise was rooted in the antithesis of what crypto evangelists believe in: one man with all the power; man over code.

There was nothing “crypto” about FTX’s business, except for the fact that they allowed you to store and buy crypto currency in exchange for fiat. Think of it this way, if a U.S. bank fails, it doesn’t mean the U.S. dollar has failed (although this could happen in parallel).

In fact, FTX operated similarly to how banks in the United States operate: they gamble your savings. The difference is that FTX did not have a license to do so, making it illegal (America’s banks have a license to do so).

Every U.S. bank takes customer deposits and lends them to other customers in the form of house loans, auto loans, etc. Most people aren’t aware that when a bank “holds” their savings, they only hold a tiny fraction of it. Usually, it’s less than 5% of what you gave them (also known as the “reserve requirement”). The bank then makes money in the form of interest on the loans they make to others.

In the event that people default on those loans, the bank has to go after the collateral, the car or house which backed the loan, and sell it in order to repay people who kept their savings in the bank. Fair or unfair, that’s showbiz, and it’s legal.

In the same vein, SBF was loaning customer deposits, albeit illegally in his case.

SBF took it a step further by:

Lending to his own entity (Alameda - his hedge fund)

Using shitcoins as collateral for loans

Betting on shitcoins with the loans

Lending to his own entity

SBF didn’t just loan deposits to random people who needed loans, but to his own hedge fund, Alameda Research. This would be like if DJ D-Sol, also known as David Solomon, CEO of Goldman Sachs, was using Goldman’s customer deposits to fund his DJ career.

Disclaimer: I saw DJ D-Sol live, and I think shitcoins are a safer use of funds.

Using shitcoins as collateral for the loans

The collateral that FTX accepted as collateral for customer deposits was not a car or a house, but FTT, the shitcoin created by FTX. No need to get into detail, but FTT broke the golden rule I laid out in last month’s newsletter: token models that involve an exchange for USD are bad news.

My last newsletter coincidentally dropped a mere 24 hours before Sam became Sam the scam. I should have gone a step further in my golden rule: token models that can be used as collateral for USD are really bad news.

Betting on shitcoins with the loans

SBF’s hedge fund wasn’t buying cars or houses with customer deposits; they were buying shitcoins, also known as non-blue chip cryptocurrencies (Solana, FTT, and others). If the value of these plummeted, which they did, something happens called a margin call, where the borrower has to cover those positions with more capital. If they don’t cover, the borrower loses the underlying collateral (in this case, the shitcoins).

This is called defaulting on your loan because you cannot pay it, and what’s left of your collateral is sold and returned to the lender (the customers of FTX). In this case, the value of the collateral (the shitcoins) is practically 0, or as they say in the World Cup, nil. This led to a $10B hole in unreturned FTX customer deposits.

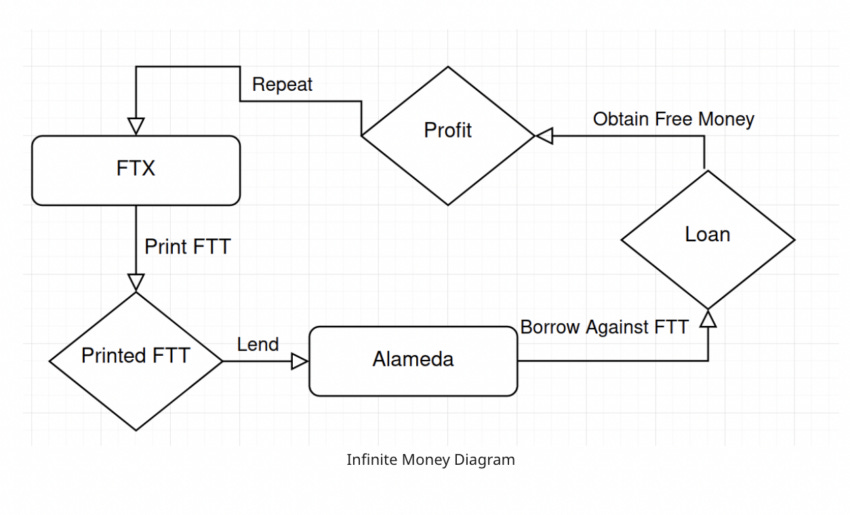

SBF took a behavior that we are already familiar with (lending customer deposits), did it illegally, and used shitcoin collateral to make risky shitcoin hedge fund bets. This diagram will help you understand the flow of funds:

Who’s being blamed, and who should be blamed?

Who’s being blamed: lemonade stands (AKA the blockchain industry)

Let’s use a simple example to explain how the media has portrayed FTX’s collapse. If the kid selling lemonade on your block happened to be pouring laxatives into the lemonade mixture, causing mass disaster across the neighborhood, should all lemonade stands be punished?

While the clear answer is no, they may be blamed anyway. Next time you go to buy street-kid lemonade, your brain will inevitably think “is it worth the risk, I should just go for the store-bought stuff, sorry kid.”

Who’s being blamed: Regulation (lack thereof)

Another media takeaway is that this happened because there aren’t enough checks and balances in crypto regulation. In our lemonade stand example, this translates to: should we be testing the lemonade stands to make sure they are selling 100% lemonade?

The answer is unequivocally yes. However, it’s important to realize that “crypto regulation” may not have stopped SBF. McKinsey & Co. famously passed on investing in Bernie Madoff after looking at his operation and sensing something fishy.

Spoiler alert: Bernie still stole the money.

Who should be blamed: SBF and his accomplices, our faulty heuristics for decision making, and VCs and others who perpetuated these faulty heuristics.

Who was to blame for Bernie Madoff stealing hundreds of millions?

Similar to FTX, many prominent people had their money with Madoff. The cooked books + perception of messianic talent was the perfect recipe for a scam.

Many, including myself, were blinded by the media, VCs, celebrity endorsements, and the aura of SBF.

The “aura” of SBF, a sloppy, poorly dressed, overweight, seemingly distracted kid, was the lynchpin. Vermeer couldn’t have painted a better tronie of a math wunderkind with limited social ability.

Some of the most successful investors on the planet invested in FTX’s private rounds, including Larry Fink of BlackRock and partners of Sequoia.

When asked if these firms did a lot of due diligence on FTX, SBF said it best: “these firms only think about upside that could be captured in future private rounds.” Meaning, if the valuation goes up for any reason, they can usually get exit liquidity, make money, and move on.

Life imitates art

SBF’s apology in his Andrew Ross Sorkin interview last Wednesday was all too reminiscent of Charles Van Doren’s closing statement in one of my favorite movies, Quiz Show. The movie recounts a true story about NBC rigging a game show to give answers to a contestant they knew would drive ratings, Charles Van Doren.

I highly recommend watching this 3 minute clip:

No one ever questioned if Van Doren knew the answers.

Similar to SBF, Van Doren was highly pedigreed, came from a prominent family, and could seemingly do no wrong (even after it came out that he CERTAINLY did wrong).

When Van Doren apologized for lying in this monologue, most of the reactions were to the tune of “wow, that was heartfelt.”

Look at the reaction from the crowd after SBF tells us he’s stolen customer deposits:

This man allegedly stole people’s money, and they clap!

Just as no one doubted Charles Van Doren, even after he was found to be lying, people still can’t seem to shift their perception that SBF is a thief. The heuristic is still broken.

Now, for my closing act, I will explain how blockchain could have averted this crisis.

Blockchain solves this

Blockchain was created to avoid the need to trust one person or entity and to increase transparency in systems.

Blockchain is frequently called a trust-less technology, and would have helped us see behind the curtains if it was used to run FTX.

Albeit a classic NYT softball interview, Andrew Ross Sorkin said it best in his interview with SBF this week: “People entrusted their funds with cryptokids doing Adderall at a slumber party. That’s not what crypto promised.”

Blockchain was supposed to mean no more Bernie Madoffs. Instead, people’s fear of decentralized systems allowed FTX to operate in an extremely centralized black box without any oversight or transparency.

There are two main caveats to trust-less blockchain systems working:

The person writing the code can be evil, so the code must be audited by many individuals. The good news is that nothing can be hidden, as it’s on the blockchain.

Codes can have errors which can cause massive financial losses which are irreversible. Intensive testing must be done to avoid this.

The goldilocks solution is somewhere in between a fully trust-less system and an all-powerful dictator. For example, the PayPal Mafia figured out that fraud protection had to be solved by first letting computers catch suspicious activity as a filtering mechanism, then having humans check their work. A similar balance will come to light here.

One example of a hugely beneficial tenet of the blockchain that could have helped avoid this disaster is ZK Proofs (Zero Knowledge proofs).

ZK Proofs

Without getting too technical, because I myself am not too technical, ZK Proofs allow people to do transactions in a trust-less manner without giving away unnecessary information. For example, if you and I make a bet for $100, you don’t need to know how much money is in my bank account, except for knowing that I have $100 to pay you if I lose. ZK Proofs are essentially a Yes/No proof of the information needed.

You can quickly see how ZK Proofs could have been EXTREMELY useful in preventing FTX’s scam. If FTX operated on the blockchain with ZK Proofs, customers could see if FTX had proof of reserves (in FTX’s case, as they are not a bank, they would have to hold 100% of customer deposits as reserves).

All in all, SBF’s demise shows us that we need to utilize aspects of the blockchain to avoid trusting autocrats that leverage the reputation systems they exist within.

En Passant Digital designs Ponzi schemes that work

Some of the biggest brands in the world trust En Passant Digital to build their incentive systems. Whether you “believe in crypto” or not is irrelevant.

Pay customers and make them stakeholders, without taking a hit to your bottom line

Better call En Passant Digital (yeah, it rhymes)

Website: enpassantdigital.com

Email: bryce@enpassantdigital.com

Thanks for reading En Passant Digital's Monthly NFT Newsletter ! Subscribe for free to receive new posts and support my work.

About the author: Bryce Baker is the co-founder of En Passant Digital, which designs and leads web3 strategy for businesses. Bryce previously worked at Parthenon-EY as a consultant for private equity firms, focusing on buying and selling technology companies.

En Passant’s other partner, John Tabatabai, has led investments for Crypto VCs and consulted for projects across the NFT space. He orchestrated one of the largest grossing NFT projects, kickstarting the first NFT bull run in early ’21, creating over $200M of value. John is designing one of the most influential Metaverse Community projects ($300M valuation at time of writing) which launches shortly.